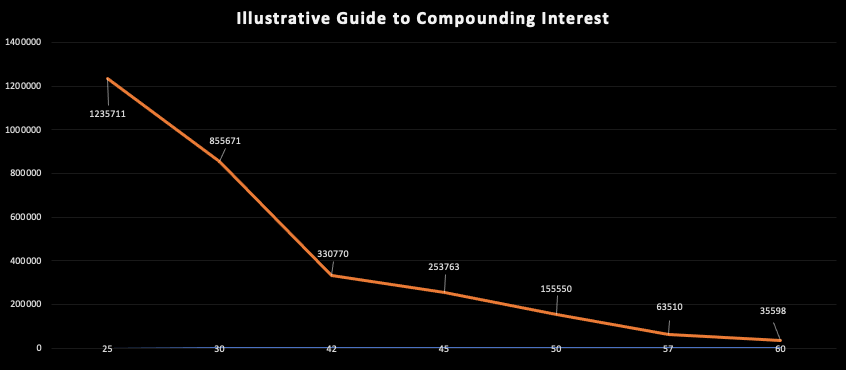

The first thing to remember when approaching investing is that the best approach is dependent almost wholly on the investor and their desired investment outcomes. While this may sound simple, working out desired outcomes hinges on many factors and conversations and ultimately works out best when a trusted financial adviser guides the investor.

In a nutshell (this is a very simple explanation):

- Active fund or portfolio management is overseen by a team of investment, market and fund specialists who make regular trades to achieve a benchmarked return.

- Passive, or index fund, management is typically where the portfolio is designed to parallel the returns of a particular market index or benchmark as closely as possible. A passive strategy does not have a management team making investment decisions and can be structured as an exchange-traded fund (ETF), a mutual fund, or a unit investment trust.

So – which is better?

When we chat about your specific needs, we will help you determine investment criteria like how much growth you need for your money and how long you have to grow it. Your perception of risk (risk appetite) and personal feelings around investing also start to come into the conversation as you consider the types of funds, stocks and companies in which you might invest. These will influence the journey we take to helping you decide which option is better suited.

What will most likely happen through this journey is that you will recognise that you have different types of investment needs: business finance, education fees, purchasing property, travel, lifestyle changes (retirement) etc.

As we develop this conversation, the need to diversify and adopt a hybrid investment approach means that we may select passive index funds for certain goals, whilst we make deliberate choices for active fund management for other investment goals.

The markets are also dynamic, as are the strategies for protecting and growing our money. Upheavals in stock markets, politics and social landscapes can change both the approach to investing as well as your financial needs. As your portfolio grows, you will also have more scope (and most likely some more appetite!) to engage in different funds and fund management.

Active funds normally have a slightly higher fee (because they anticipate better returns) whilst passive funds are more cost-effective. Ultimately, the markets and the future are not sure-things, which is why a balanced and well-thought-out approach is always advisable.